Management control systems (such as budgets or balanced scorecards) are formal procedures used by managers to promote employee behavior aligned with organisational objectives. Employees may react to these control systems by either becoming more motivated or perceiving them as a threat. The aim of this paper is to determine the extent to which hospital ownership (public or private), professional group (physician, nurse, pharmacist or administrative employee), type of contract (fixed or temporary), gender and tenure can condition employee reaction to management control systems.

MethodsWe conducted the study in the three largest hospitals in the State of Santa Catarina (Brazil), two public (federal and state-owned) and one private (non-profit organisation). Physicians, nurses, pharmacists and administrative employees received a questionnaire between October 2013 and January 2014 concerning their current perceptions. We obtained 100 valid responses and conducted an ANOVA variance analysis.

ResultsOur results show that the effect of management control systems on employees differs according to hospital ownership, professional group and type of contract. However, no significant evidence was found concerning gender or tenure.

ConclusionsThe results obtained contribute to creating specific knowledge on the reactions of employees to the use of management control systems in hospitals. This information may be important in adapting management control systems to the characteristics of the hospital and its employees, which may in turn contribute to reducing dysfunctional worker behavior.

Los sistemas de control de la gestión (p. ej., presupuestos o cuadro de mando integral) son prácticas formales que utilizan los directivos para promover que los empleados desarrollen comportamientos alineados con los objetivos de la organización. Los empleados pueden percibirlos como una fuente tanto de motivación como de amenaza. El objetivo de este trabajo es determinar si la propiedad del hospital (pública o privada), el grupo profesional (médico, enfermera, farmacéutico o administrativo), el tipo de contrato (indefinido o temporal), el género y la permanencia en el puesto condicionan la reacción del empleado ante un sistema de control de gestión.

MétodoEl estudio se realizó en los tres mayores hospitales del Estado de Santa Catarina (Brasil), dos públicos (federal y estatal) y uno privado (no lucrativo). Entre octubre de 2013 y enero de 2014 se envió una encuesta sobre percepciones presentes a médicos, enfermeras, farmacéuticos y administrativos. Se realizó un análisis ANOVA a partir de 100 respuestas válidas para este estudio.

ResultadosLos resultados muestran que el efecto de los sistemas de control de gestión sobre los empleados es diferente en función de la propiedad del hospital, el grupo profesional y el tipo de contrato. Sin embargo, no se encontró evidencia significativa en relación con el género ni a la permanencia en el puesto.

ConclusionesLos resultados obtenidos contribuyen a crear un conocimiento específico de las reacciones a los sistemas de control en los hospitales. Esta información es relevante para adaptar el sistema de control al hospital y sus empleados, reduciendo así comportamientos disfuncionales.

Changes in the health environment have affected the performance and economic and financial management of health institutions, mainly hospitals.1 Improving the health quality and the services provided by hospitals requires promoting employee behavior aligned with organizational objectives, and avoiding selfish conducts that place personal interests before those of the organization.1 Some of the behavior acknowledged in the healthcare literature are: low commitment to organizational goals,1–3 fraud and corruption,4,5 conflicts,6 or unethical behavior.7

Among other strategies,8 managers may use management control systems (MCS) to assure that professionals behave according to the objectives of the organization.9 The most common MCS used in hospitals are the balanced scorecard,10,11 budgeting systems,12,13 and cost control.14,15 The growing literature over the last decades on the use of MCS in health institutions16 provides evidence on the positive consequences of implementing these tools to direct hospital employee behavior. Findings suggest that MCS may promote cooperation and coordination,12 cost containment17 or participation.18 On the one hand, MCS may contribute to guiding the conduct of professionals by informing and motivating them to do what the organization expects of them.19,20 On the other hand, MCS may contribute to guiding the behavior of employees by informing them about the negative consequences of behaviors that are unacceptable to the organization, i.e., MCS may be perceived as a threat.1,21 In brief, employees may react to MCS by either becoming more motivated and/or perceiving these measures as a source of threat.

This study aims to analyze the specific reactions of health professionals to MCS. Literature in psychology notes that organizational factors and individual characteristics are paramount to understanding employee reactions to certain circumstances.22 Fundamentally, our study argues that the reaction (motivation and/or threat) of an employee to MCS is conditioned by hospital ownership (public or private hospital), the professional group (physician, nurse, pharmacist or administrative), the type of contract (fixed or temporary), the gender and the tenure (years of professional experience). On the one hand, organizational factors such as ownership or professional group are expected to influence employee reaction to MCS given the different backgrounds, norms and values among these groups.23,24 On the other hand, individual characteristics such as type of contract, gender and tenure may also play a key role due to diverse socialization processes, levels of commitment and intrinsic motivation.20

MethodsThis study is part of a broader international project related to management in hospital organizations. Here we present quantitative research, conducted through a survey distributed among the employees of the three largest hospitals in the State of Santa Catarina (Brazil). Brazil is amongst the countries that hold a universal public health care system. The Brazilian Constitution establishes a minimum percentage of 15% of the net current revenue of the financial year for health. By 2014, 71% of the population (approximately 142 million) went to public health facilities for care. The total resources invested in public health actions and services accounted for approximately US $30 billion. On the other side, 50 million private health plans were contracted in Brazil in 2014.25 Regarding managerial practices, the Brazilian Health Ministry (Ministérioda Saúde) designs MCS that hospitals are expected to implement. Such is the case, for example, of a recent computerized system for cost accounting. The effective design, implementation and use of MCS in Brazilian hospitals is currently an issue among managers, government and academics in Brazil.26–28

The questionnaire was designed following the suggestion of Dillman.29 Before administering the questionnaire, we conducted a pre-test. We first contacted six academics with experience in the area to provide a pretest. After receiving expert advice and doing proposed revisions, we pre-tested three professionals from the healthcare sector to check potential weaknesses, like confusing instructions, unintelligible questions or excessive time devoted to completing the survey. We obtained valuable suggestions from this process and incorporated them into the final version of the questionnaire. Scientific committees from the three hospitals approved the project and the questionnaire. One of them was a private non-profit organization (198 beds), another was a state-administered public hospital (329 beds) and the third was a public hospital school administered by the federal government (228 beds).

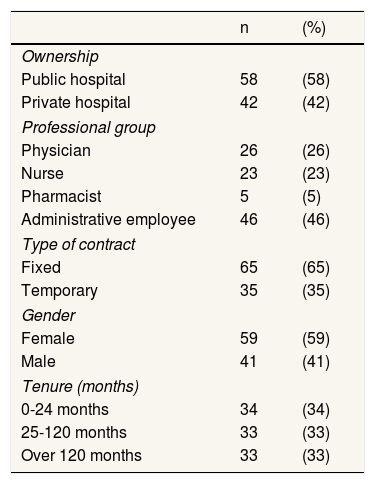

The period in which the questionnaires were sent and collected includes the months of October 2013 through January 2014. The questionnaire was anonymous and followed by a letter explaining the project and an acknowledgement note for the participation. Once this was all completed it was collected and put into a box that was properly elaborated for its return with no trace of identification. The aim of this procedure was to avoid external interference to the respondent employees, i.e. avoid any embarrassments or pressure on the employees. Initially, 135 complete questionnaires were received (29.67% of the population). Some questionnaires lacked significant data and could not be used in this study. The survey resulted in 100 usable responses for this study. Table 1 displays the demographic data of the sample. Top and middle managers were excluded from the sample due to the possibility of a biased perception of control given that these managers are the ones that usually design, implement and use MCS. Professionals with no managerial roles are in the group of administrative employees from different departments within the hospital such as accounting, human resources or IT.

Descriptive statistics of the sample (N=100).

| n | (%) | |

|---|---|---|

| Ownership | ||

| Public hospital | 58 | (58) |

| Private hospital | 42 | (42) |

| Professional group | ||

| Physician | 26 | (26) |

| Nurse | 23 | (23) |

| Pharmacist | 5 | (5) |

| Administrative employee | 46 | (46) |

| Type of contract | ||

| Fixed | 65 | (65) |

| Temporary | 35 | (35) |

| Gender | ||

| Female | 59 | (59) |

| Male | 41 | (41) |

| Tenure (months) | ||

| 0-24 months | 34 | (34) |

| 25-120 months | 33 | (33) |

| Over 120 months | 33 | (33) |

Using the chi-square statistics, we found no significant differences (p>0.01) among early and late participants (first 20% responses to late 20% responses). To detect the presence of common method bias, we plotted all the variables simultaneously on an exploratory factorial analysis. Harman's single factor test30 assumes a strong evidence of common bias if a single or common factor is found on the factor analyses; this captures most of the covariance among the variables. Moreover, results suggest 8 factors with eigenvalues higher than 1; this explains 74.15% of the total variance, while the first factor only accounts for 28.42% of the variance. The first factor explains less than half of the over-all variance so the results are subject to no common bias.

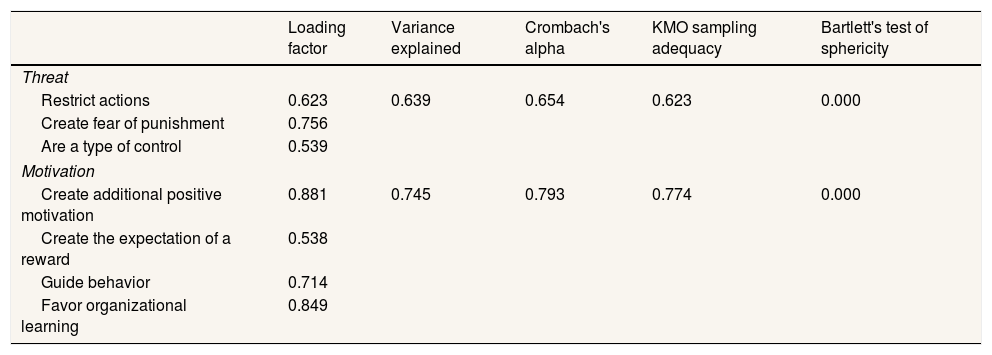

The main issue regarding the reactions to MCS is based on the proposal by Tessier and Otley,19 constituted by seven questions with a seven-point scale (1: completely disagree; 7: completely agree). The questions were related to when MCS: (i) restrict actions, (ii) create fear of punishment, (iii) are a type of control, (iv) create additional positive motivation, (v) create the expectations for a reward, (vi) guide behavior, and (vii) favor organizational learning.

Items from (i) to (iii) were used to measure the MCS perceived by the professional as a real tangible threat. That is, professionals understand MCS as an indication that they should avoid certain behaviors or activities contrary to organizational goals. For example, if expenses in certain budgeting accounts are exceeded, they may be penalized. On the other hand, motivation was measured through items from (iv) to (vii). That is, professionals realize that something must be done to attain organizational goals. Such is the case, for example, when a goal motivates professionals to use generic drugs that may reduce the operational expenses of the hospital.

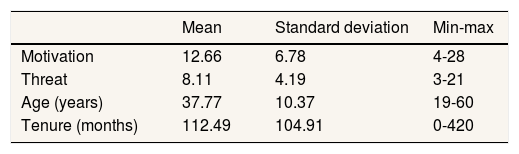

Table 2 analyzes the validity and reliability of motivation and threat scales exceeding the cut-values.31 We created a summated scale for each construct by adding the scores of the proposed items. Table 3 shows a descriptive statistical analysis. We used SPSS software (Statistical Package for the Social Sciences), version 22, to analyze the data.

Factor analysis of reflective constructs (N=100).

| Loading factor | Variance explained | Crombach's alpha | KMO sampling adequacy | Bartlett's test of sphericity | |

|---|---|---|---|---|---|

| Threat | |||||

| Restrict actions | 0.623 | 0.639 | 0.654 | 0.623 | 0.000 |

| Create fear of punishment | 0.756 | ||||

| Are a type of control | 0.539 | ||||

| Motivation | |||||

| Create additional positive motivation | 0.881 | 0.745 | 0.793 | 0.774 | 0.000 |

| Create the expectation of a reward | 0.538 | ||||

| Guide behavior | 0.714 | ||||

| Favor organizational learning | 0.849 | ||||

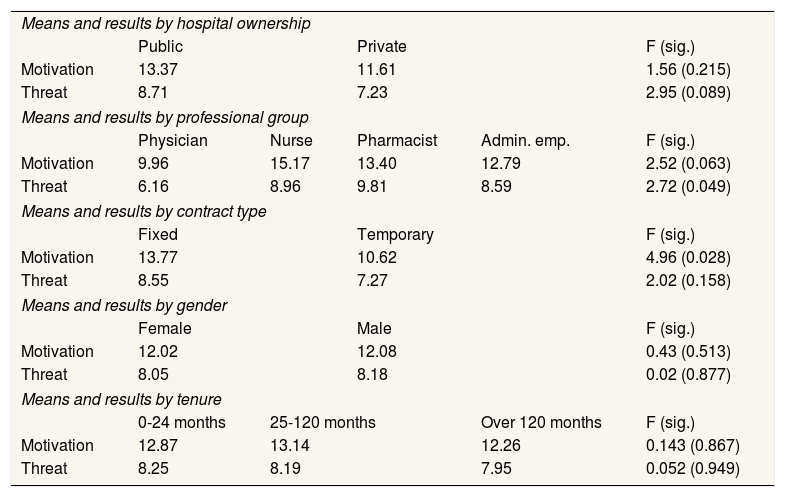

Table 4 presents results about the employee reactions to MCS according to hospital ownership, professional group, type of contract, gender and tenure. Firstly, regarding hospital ownership, Table 4 shows higher motivation and threat on public hospitals in relation to private ones, although this difference is only significant in threat perception.

ANOVA means and results.

| Means and results by hospital ownership | |||||

| Public | Private | F (sig.) | |||

| Motivation | 13.37 | 11.61 | 1.56 (0.215) | ||

| Threat | 8.71 | 7.23 | 2.95 (0.089) | ||

| Means and results by professional group | |||||

| Physician | Nurse | Pharmacist | Admin. emp. | F (sig.) | |

| Motivation | 9.96 | 15.17 | 13.40 | 12.79 | 2.52 (0.063) |

| Threat | 6.16 | 8.96 | 9.81 | 8.59 | 2.72 (0.049) |

| Means and results by contract type | |||||

| Fixed | Temporary | F (sig.) | |||

| Motivation | 13.77 | 10.62 | 4.96 (0.028) | ||

| Threat | 8.55 | 7.27 | 2.02 (0.158) | ||

| Means and results by gender | |||||

| Female | Male | F (sig.) | |||

| Motivation | 12.02 | 12.08 | 0.43 (0.513) | ||

| Threat | 8.05 | 8.18 | 0.02 (0.877) | ||

| Means and results by tenure | |||||

| 0-24 months | 25-120 months | Over 120 months | F (sig.) | ||

| Motivation | 12.87 | 13.14 | 12.26 | 0.143 (0.867) | |

| Threat | 8.25 | 8.19 | 7.95 | 0.052 (0.949) | |

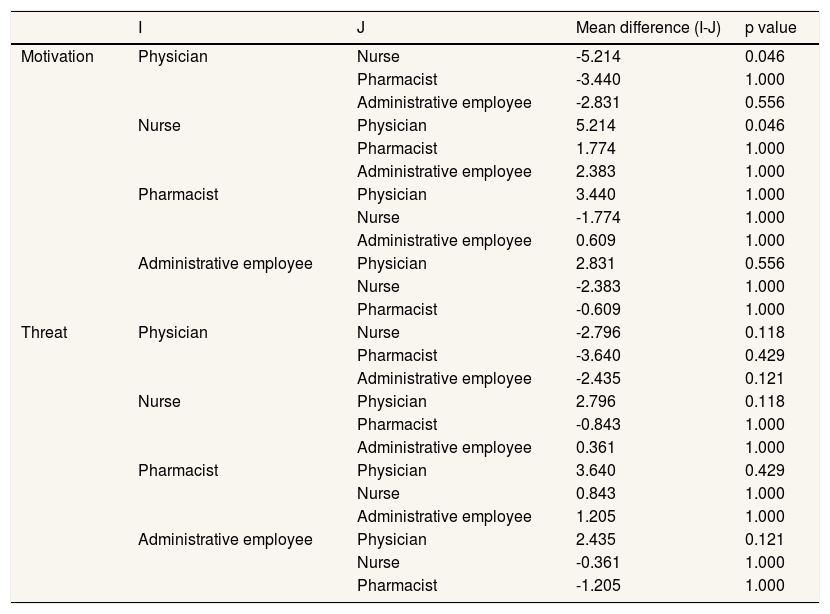

Secondly, we analyze employee reactions to MCS by professional group. Regarding motivation, nurses are the professionals that show the highest values, while physicians show lower values, with significant differences of 10%. Lastly, in relation to threat, pharmacists are the group with the highest scores, while physicians are the professionals with the lowest values (significant differences at 5%). We also analyze differences by pairs using a Bonferroni test (Table 5). We only observe significant differences in motivation perception between physicians and nurses (at 5% level).

Bonferroni test on professional group.

| I | J | Mean difference (I-J) | p value | |

|---|---|---|---|---|

| Motivation | Physician | Nurse | -5.214 | 0.046 |

| Pharmacist | -3.440 | 1.000 | ||

| Administrative employee | -2.831 | 0.556 | ||

| Nurse | Physician | 5.214 | 0.046 | |

| Pharmacist | 1.774 | 1.000 | ||

| Administrative employee | 2.383 | 1.000 | ||

| Pharmacist | Physician | 3.440 | 1.000 | |

| Nurse | -1.774 | 1.000 | ||

| Administrative employee | 0.609 | 1.000 | ||

| Administrative employee | Physician | 2.831 | 0.556 | |

| Nurse | -2.383 | 1.000 | ||

| Pharmacist | -0.609 | 1.000 | ||

| Threat | Physician | Nurse | -2.796 | 0.118 |

| Pharmacist | -3.640 | 0.429 | ||

| Administrative employee | -2.435 | 0.121 | ||

| Nurse | Physician | 2.796 | 0.118 | |

| Pharmacist | -0.843 | 1.000 | ||

| Administrative employee | 0.361 | 1.000 | ||

| Pharmacist | Physician | 3.640 | 0.429 | |

| Nurse | 0.843 | 1.000 | ||

| Administrative employee | 1.205 | 1.000 | ||

| Administrative employee | Physician | 2.435 | 0.121 | |

| Nurse | -0.361 | 1.000 | ||

| Pharmacist | -1.205 | 1.000 |

Thirdly, we analyze employee reactions to MCS according to type of contract. Fixed employees showed higher motivation and threat reactions than did temporary employees, although only the first one is significant (at 5%), according to Table 4.

Fourthly, we analyze employee reactions to MCS by taking gender into account. Male employees showed higher motivation and threat reactions than did female employees; although neither of them show significant effects (Table 4).

Finally, we test the relationship between tenure and the employee reactions to MCS.32,33 The results of this comparison show no significant differences (Table 4).

ConclusionsThe effectiveness of MCS in terms of consequences on employee behavior is currently one of the major challenges to hospital organizations.13,20 In this line, drawing on a sample of 100 respondents, this study aims to determine the extent to which organizational factors (hospital ownership and professional group) and individual characteristics (type of contract, gender and tenure) can condition employee reaction (motivation or threat) to MCS. Our results present central questions that should be discussed within the context of the existing literature.

Regarding hospital ownership, we observed that employees from public hospitals show higher levels of threat than do employees from private hospitals. This finding falls in line with previous research suggesting public employees are less satisfied with their supervisors and hold weaker distributive and procedural justice perceptions.34 Therefore, this paper sheds some light on the conceptualization of the differences between public and private organizations, an issue still debated among researchers.35 Besides, and also related to organizational factors, results that we initially obtained by comparing the values of the four groups of employees seem to be consistent with those of previous literature that stress the differences among non-clinical and clinical staff based on their different individual backgrounds.36 However, when going deeper into our analysis and refining it, we observe that the significant differences are limited to those between physicians and nurses. The latter shows higher levels of motivation. One plausible argument is that physicians are intrinsically motivated professionals;20 thus MCS cannot perform all of its postulated features.

Regarding individual variables, fixed employees present significantly higher levels of motivation reactions than do temporary employees. This result is consistent with previous research that suggests that the type of contract is directly related with job satisfaction and organizational commitment.33,37 However, as opposed to expectations, our findings suggest that gender and tenure are irrelevant. This lack of effects does not support arguments drawing on socialization, motivation, and equity theories in favor of a gender and tenure effect on employee behavior.38,39

In conclusion, our results fall in line with previous literature defending the need to distinguish between the intentions of managers implementing a MCS and the reactions developed by the professional in terms of the MCS.19 Moreover, the findings may draw the attention of organizations and managers to the importance of the aspects studied herein when designing and implementing a MCS in a hospital.1,11,13 Hospital managers must analyze and adapt the design and implementation of MCS tools to the characteristics of the organization and the professionals potentially subject to control.20 Otherwise, the use of MCS may be inefficient or show results contrary to those expected. The use of MCS may be unfair, and professionals could see it as such. This would create a situation of minimal congruence, since the professionals do not identify with the system and, consequently, with the objectives of the organization. In addition, a negative perception may damage its value, since the professionals could participate in behaviors potentially harmful to the organization.16

This paper has several limitations. First, as other studies in healthcare management literature,40 the data analyzed comes from a reduced number of hospitals in a specific geographic area marked by some very particular sociocultural specificities. Future research may use a larger multinational sample. This would allow it to shed more light on perceptions of control within hospitals. This limitation implies that one should interpret the results with care. A further limitation comes from the nature and the small number of variables considered in our research model. New organizational and individual variables such as internal process control or organizational culture would complete our analyses. Moreover, measures of individual and organizational performance would allow an analysis of the implications of motivation, threat and the interaction of both. Finally, the institutional environment of hospitals includes multiple stakeholders who may interact at some point with MCS. This was missing in this study. In this sense, we recommend that future researchers consider new perspectives from internal and external stakeholders such as hospital managers, patients or pharmaceutical representatives.

Studies on hospitals settings support the idea that the use of Management Control Systems promotes employee behaviors aligned with organizational objectives that may lead on successful implementation of business strategies and on gaining efficiencies.

What does this study add to the literature?This study further examines and clarifies how the use of management control systems may guide employee behavior. Employee reactions to management control systems can be: motivation, threat or both. We found that these reactions are significantly different according to the hospital ownership, the professional group, and the type of contract.

David Cantarero.

Transparency declarationThe corresponding author on behalf of the other authors guarantee the accuracy, transparency and honesty of the data and information contained in the study, that no relevant information has been omitted and that all discrepancies between authors have been adequately resolved and described.

Authorship contributionsAll authors were involved in the conception, design and writing of the manuscript. E. Lopez-Valeiras and R.J. Lunkes supervised the data collection. J. Gomez-Conde carried out the data analysis. E. Lopez-Valeiras and J. Gomez-Conde interpreted the data and critically reviewed the manuscript. All authors have approved the final version of the manuscript.

FundingWe acknowledge the financial contribution from Fundación COTEC-Programa de Innovación Abierta 2016 (PIA) and the Spanish Ministry of Economy, Industry and Competitiveness (ECO2016-77579-C3-3-P; ECO2014-56204-P).

Conflicts of interestsNone.

We would like to acknowledge the support of Banco Santader under program “Becas Iberoamérica, Jóvenes Profesores e Investigadores, Santander Universidades” (España, 2013), the assistance in the data collection provided by Mauricio Vasconcellos Leão Lyrio, and the English revision service provided by Carmen Negreira.